To Our Investors and Friends,

The S&P 500 fell .2% in January as a combination of Corona Virus and an impeachment trial spooked the market at the end of the month. Oil prices (WTI) plummeted almost 16% to $52 a barrel as concerns over a slowdown in China dominated the commodity. The 10-year dropped 37 basis points during the quarter to end at 1.51%, a level not seen since last fall. The spread between the 2- and 10-year fell to 18 bps. Large companies performed far better than small. The Russell 1000 Growth led the market, up 2.24% driven by strong tech earnings. This far exceeded the 2.15% decline in the Russell 1000 Value, as financials and industrials gave back some gains earned at the end of last year. In the small cap space, the Russell 2000 Growth fell 1.1% and the Russell 2000 Value dropped 5.4%.

Earnings season has begun and is largely revealing continued strong growth for many new sectors of the economy, led by technology companies such as Microsoft (MSFT) and Apple (AAPL), and continued weakening trends in many industrials – most recently Boeing (BA) and Caterpillar (CAT). Not surprisingly, the stock market is again reflecting these underlying trends.

Over the last decade, the number of quantitative strategies available to investors has exploded. Many of them rely on price momentum as a primary factor in their algorithms from which they base their buy and sell decisions. We are seeing early in 2020 that not all price momentum is the same. In fact, speculative price momentum, in which market price is anticipating a change in trends, drove the performance of industrials and financials in the last few months of 2019. This is price momentum using a fragile material such as straw as its foundation…. quick to construct, and equally quick to fall apart. Price momentum built on fundamentals is using brick as its foundation…it often takes longer to build, but is far more durable as market fears materialize. In fact, Robert Novy-Marx’s paper Fundamentally, Momentum is Fundamental Momentum (https://www.nber.org/papers/w20984) points out that earnings momentum is the primary determinant of stock momentum, and that price momentum strategies absent of earnings momentum give investors high volatility without better performance.

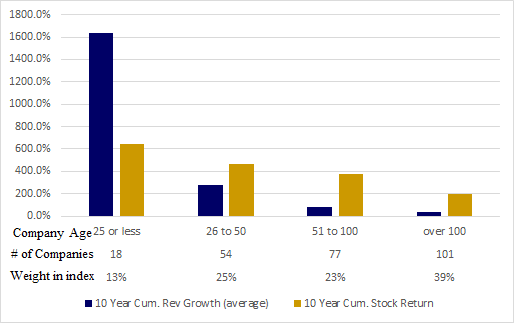

Our search continues for transformational businesses…those companies that offer superior solutions to what currently exists. Such companies generally experience rapid revenue growth that eventually leads to even faster earnings growth, although oftentimes later in the company’s life cycle. Next generation businesses are using a customer-centric approach that leads to predictable, ongoing customer relationships that produce steady revenue and earnings growth over a span of years. In the end, these strong customer relationships are the bricks used to build predicable revenue and earnings streams that lead to higher stock prices over time.

All the Best to You,

AKW